When Fines Replace Accountability: The NSE Settlement and the Arithmetic of Absurdity

- Rajangam Jayaprakash

- Apr 23

- 3 min read

The proposed settlement between the National Stock Exchange of India (NSE) and the Securities and Exchange Board of India (SEBI) is being presented as closure. In formal terms, it fits within a consent-based enforcement architecture. In economic terms, however, it raises a sharper question:

Has a multi-year structural distortion of market fairness been reduced to a financially efficient exit?

A tighter reading—through the lenses of time horizon, beneficiary concentration, gain extraction, and penalty proportionality—suggests that the answer may be yes.

I. The Structural Period: Advantage as a Regime

Between roughly 2010–2014, the co-location architecture enabled:

Preferential access to order book data

Faster tick-by-tick feeds

Server-level login advantages

This was not episodic misconduct. It was a persistent microstructure asymmetry.

Visual 1: Nature of Advantage

Standard Market Participant Privileged Participant

--------------------------- -----------------------

Normal latency ↓ Lower latency

Delayed data access ↓ Early data visibility

Queue disadvantage ↓ Queue priority

Outcome: Neutral market Outcome: Systematic edge

In high-frequency markets, this translates directly into economic rent extraction.

II. Beneficiary Set: Narrow but Powerful

Regulatory focus has consistently pointed to a small cluster of high-frequency firms (single-digit to low double-digit participants).

These entities were:

Technologically sophisticated

Capital efficient

Strategically positioned

They were not incidental beneficiaries—they were optimal extractors of structural advantage.

III. Economic Extraction Model

To understand proportionality, one must first understand how gains scale.

Visual 2: Gain Mechanics

Micro Advantage per Trade (₹) → High Trade Volume → Multi-Year Duration

↓ ↓ ↓

Small Edge Thousands/day 4–5 years

↓

Compounded Gains

↓

₹100s of crores (plausible)

Even conservative assumptions yield large cumulative gains per participant.

IV. Penalty Structure: Finite vs Compounding

Observed enforcement outcomes:

Aggregate penalties → Hundreds of crores

Individual penalties → ₹1–30 crore range (typical cases)

Visual 3: Asymmetry

GAINS (Dynamic) PENALTIES (Static)

----------------- -------------------

Compounding One-time

Market-linked Regulator-defined

Multi-year Single event

Uncapped Capped

Result: Gains >> Penalties

V. The Deterrence Test (Fails Quietly)

A basic enforcement condition:

Expected Penalty ≥ Expected Gain

In this case:

If: Gain (₹200–500 Cr) > Penalty (₹5–20 Cr)

Then: Violation remains economically rational

This transforms enforcement into post-facto pricing, not deterrence.

VI. The Institutional Pivot

After participant-level penalties, the system arrives at:

👉 NSE paying a large settlement to SEBI

This is where the economic logic fractures.

VII. Ownership Reality: Who Actually Pays?

The NSE’s shareholding includes:

Life Insurance Corporation of India

State Bank of India

Stock Holding Corporation of India

This implies:

A meaningful portion of NSE capital is publicly anchored

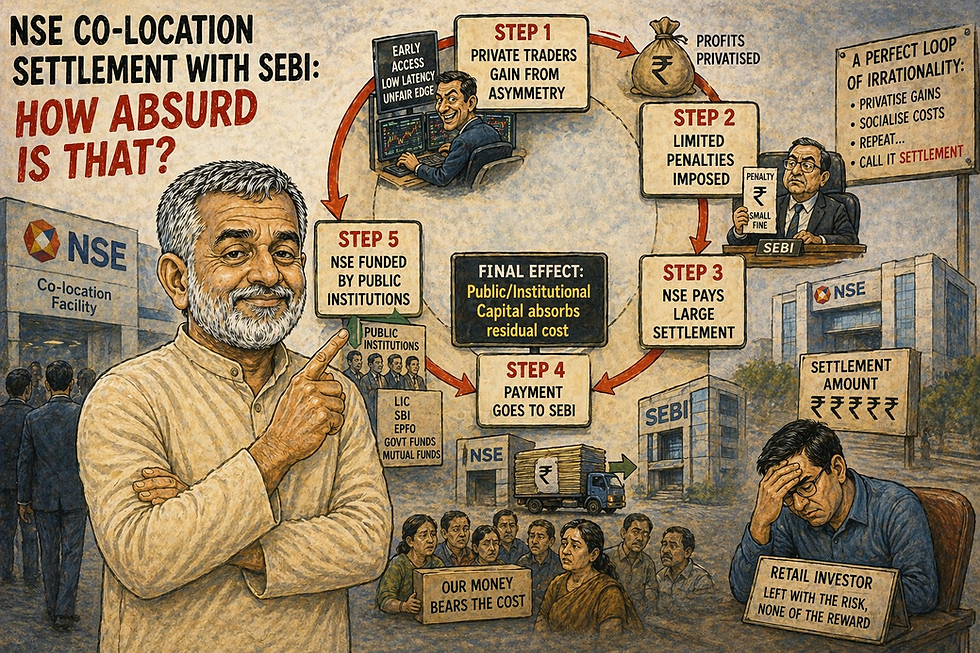

VIII. The Circular Flow of Accountability

Visual 4: The Full Loop

Step 1: Private Traders gain from asymmetry

↓

Step 2: Limited penalties imposed

↓

Step 3: NSE pays large settlement

↓

Step 4: Payment goes to SEBI

↓

Step 5: NSE funded by public institutions

FINAL EFFECT:

Public/Institutional Capital absorbs residual cost

Interpretation

Private gains → partially penalized

Residual burden → socialized via NSE

State → receives payment from state-linked capital

This is not just irony. It is circular enforcement economics.

IX. The IPO Overlay

Settlement timing aligns with NSE’s long-delayed listing ambitions.

Visual 5: Incentive Alignment

Pending Cases → Settlement Payment → Clean Balance Sheet → IPO Readiness

This raises a difficult question:

Is the objective enforcement completeness—or transaction readiness?

X. Conceptual Shift: From Prohibition to Pricing

When:

Gains are not fully clawed back

Penalties are not binding

Institutions absorb residual costs

The system implicitly moves from:

“Do not violate”

↓

“If you do, this is the cost”

This is a first-order moral hazard.

XI. What a Coherent Framework Would Require

Visual 6: Ideal vs Observed

IDEAL SYSTEM OBSERVED SYSTEM

-------------- ----------------

Full disgorgement Partial penalties

Individual accountability Institutional settlement

Gain-linked penalties Fixed fines

Deterrence Pricing mechanism

XII. Final Synthesis: The Arithmetic Doesn’t Close

The NSE settlement delivers closure—but not equilibrium.

The imbalance:

Extraction → Multi-year, compounding, private

Penalty → Finite, capped, partial

Final Cost → Institutional, diffuse, partly public

Closing Line

The issue is not that a fine is being paid.It is that:

The gains were private, the penalties were limited, and the closure is being funded—at least in part—by public capital.

That is not merely a regulatory outcome.It is a misalignment of economic accountability—precisely in the institution tasked with ensuring market fairness.

Comments